Recently, Sky News with their Economics and Data Editor Ed Conway, released an incredibly interesting and insightful video on the state of UK gas and oil, thoughtfully entitled: ‘Is Britain Sitting on More Gas?’ but, did it miss the point…?

Recently, Sky News with their Economics and Data Editor Ed Conway, released an incredibly interesting and insightful video on the state of UK gas and oil, thoughtfully entitled: Is Britain Sitting on More Gas?

The video is certainly compelling and makes some strong points on historic UK gas and oil production, alongside projected supply and demand figures beyond 2035, suggesting that declining “cult chart” figures aren’t anywhere near as dire as they might first seem, supported, crucially by the idea that – actually – there is still a lot of gas left to mine in North Sea Gas Fields that should and could be utilised.

Essentially, Conway’s analysis for Sky News outlines a critical “Gas Gap” facing the UK as it transitions away from fossil fuels, touching on the UK government’s refusal to issue licences which would increase projected UK gas production considerably whilst bringing down future gas prices and lowering demand for “risky” and expensive imported gas and LNG.

Key Stats: Is Britain Sitting on More Gas?

There are certainly many interesting touch points to consider as part of Conway’s analysis, including:

46% of our gas to come from LNG by 2035: The UK has moved from being a net exporter in 2000 to a heavy importer today and, by 2035, if current trends continue, 46% of our gas will come from Liquefied Natural Gas (LNG) shipped from places like Qatar and the US. This high dependency on LNG is not just a security risk; it is also more carbon-intensive than domestic production.

Projections were more optimistic a few years ago: A “cult chart” circulating in Whitehall shows North Sea production falling precipitously. Interestingly, projections from just a few years ago were much more optimistic, and the video suggests that the recent sharp decline in these forecasts is tied to the new government’s ban on new licenses and exploration.

Domestic drilling might actually be better for the environment than importing: Importing gas as a liquid on tankers emits roughly 27kg of CO2 per barrel equivalent whereas keeping production in the North Sea reduces the transport and liquefaction emissions, potentially lowering the total carbon footprint of the gas we must still use during the transition.

US gas prices have plummeted in recent years: due to fracking initiatives, US gas prices have plummeted in recent years and, in fact, fracking has turned the US into the world’s largest gas producer. Because the US has massive internal pipeline networks and was (until recently) limited in how much it could export, domestic supply overwhelmed domestic demand, causing prices to “plummet” compared to the rest of the world.

Production reality: UK gas output has hit record lows in early 2026, dropping faster than the rate of decarbonisation in home heating and industrial use.

However, what Conway’s analysis doesn’t go into and, indeed, hardly touches on, is the role of renewable and clean energy projects in the UK’s projected gas production and our government’s conscious move to turn away from fossil fuel derived energy to renewable and clean energy in order to bridge the “Gas Gap” and achieve energy independence; thus making some of these key stats and takeaways counter intuitive.

The UK’s Conscious Move Away From Fossil Fuels

For many years now, the UK has been moving away from fossil fuels and towards renewable, clean and low carbon energy sources, working to consciously de-incentivise fossil fuel derived gas and oil, and incentivise renewable and clean energy projects such as solar farms, wind farms, green hydrogen production, and nuclear power plants.

To support this pivotal energy strategy, our government has implemented a “windfall tax” on gas and oil companies of 38% – bringing the total effective tax rate on North Sea producers to 75% – which has been extended to 2030.

This tax, which is understandably looked upon unfavourably by the gas and oil sector(s) – and is worth billions of pounds – is injected into the National Wealth Fund and used to mobilise projects like Carbon Capture Usage and Storage, Hydrogen and green infrastructure.

And, whilst this fiscal pivot successfully accelerates the long-term transition, it creates an immediate “Baseload Gap” because intermittent sources like wind and solar are the backbone of our future grid, but they cannot yet replace the steady, “always-on” reliability of the gas we are moving away from.

Furthermore, as the North Sea’s managed decline accelerates, we risk trading domestic energy for high-carbon, high-cost LNG imports to keep the lights on during periods of low wind or sun.

What’s more, and as Conway’s analysis investigates, where around 80% of North Sea gas has already been successfully mined and used, there is only 20% left.

Taking this point further, of that 20% left, most of it is “hard to reach” meaning that the cost of extracting it vs. the yield it is expected to produce makes it, frankly, not worth it – i.e. we simply won’t get enough of it to justify the high cost of mining for it.

But this is where Energy from Waste (EfW) and Anaerobic Digestion (AD) could very well represent the missing piece of the UK’s current and future energy puzzle and something that wasn’t highlighted in Sky News and Conway’s report.

Could Energy from Waste and AD Bridge the Gas Gap?

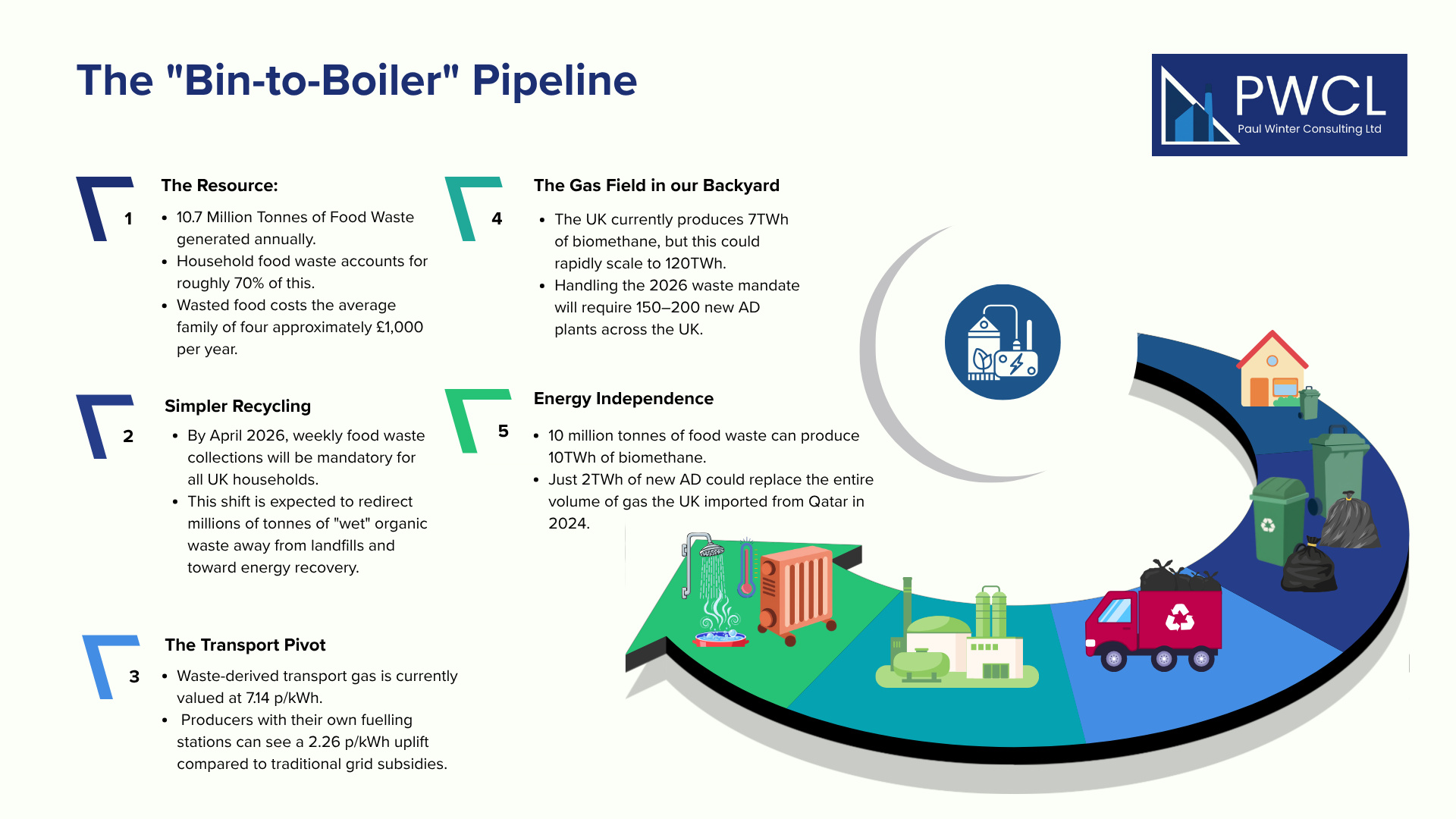

Particularly given the UK’s forthcoming move to Simpler Recycling in April 2026 and mandated weekly food waste collections, Energy from Waste and – in particular – Anaerobic Digestion could very well hold the key to solving the UK’s energy security issues and earn their rightful places as cornerstone solutions to long-term [energy] self-sufficience and meaningful waste management.

This is because the UK generates between 9.5 and 10.7 million tonnes of food waste every year and household (AKA domestic) food waste accounts for around 60-70% of this total, or approximately 6.6 million tonnes.

With this, edible food waste here in the UK comes with a significant economic loss, as it costs the UK approximately £17 – 19 billion annually, or £1000 for a family of four, whilst also accounting for 18 million tonnes of CO2 equivalent, about 3% of total UK greenhouse gas emissions.

And, when it comes to biomethane, the UK currently produces approximately 7 TWh of biomethane annually, but industry experts (such as ADBA) suggest this could rapidly scale to 120 TWh, potentially meeting 20% to 50% of long-term UK gas demand.

This would mean that, by next winter, an additional 2 TWh could be brought online which is enough to replace the entire volume of gas the UK imported from Qatar in 2024.

Alongside this and unlike hydrogen, biomethane is chemically identical to natural gas; it uses existing pipes and boilers, making it the fastest way to “green” the gas grid without expensive retrofits, meaning that we don’t have to significantly change the grid in order to accommodate it – that is, beyond the necessary and already planned & budgeted for grid maintenance and upgrades currently in the works.

10 million tonnes of food waste produced, when processed via AD, 10 million tonnes can produce ~10 TWh of biomethane – enough to power 800k+ homes – where biomethane is a “drop-in” replacement for fossil gas and requires no new infrastructure for use.

While Anaerobic Digestion is the optimal route for 10 million tonnes of “wet” food waste, the benefits of the April 2026 Simpler Recycling mandate extend directly into the UK’s Energy from Waste (EfW) infrastructure.

Currently, when food waste is mixed into general “black bag” bins, it acts as a thermal sponge, and because food is roughly 70–80% water, EfW incinerators must expend significant energy just to evaporate that moisture before the remaining waste can actually burn.

This lowers the Net Calorific Value (NCV) – essentially the “fuel quality” – of the entire waste stream.

By mandating separate food waste collections, the UK is effectively “drying out” its residual waste, creating a dual-win for energy security:

For EfW: Removing the “wet” organic fraction allows incinerators to operate at higher efficiencies, where the remaining dry waste (plastics, paper, textiles) burns hotter and more consistently, allowing EfW plants to generate more electricity and heat per tonne of waste processed.

For the Grid: We stop wasting energy “boiling” food in incinerators and start harvesting that same food for 10 TWh of biomethane in AD plants.

Together, these two technologies form a robust, domestic energy shield.

While AD provides the dispatchable green gas needed to replace North Sea imports, a “streamlined” EfW sector provides the baseload electricity needed to support an increasingly electrified UK.

By April 2026, we won’t just be managing waste more effectively; we will have the infrastructure to move from a system of “disposal” to a sophisticated “Biomass-to-Energy” refinery, where every tonne of waste is directed to the technology that can extract the maximum possible value.

However, there is a figurative “spanner in the works” when it comes to the practical implementation of this otherwise heterotopian projection…

The “Spanner in the Works”: GGSS Paradox

The implementation of mandatory weekly food waste collections by 31st March 2026 is designed specifically to redirect these 10 million tonnes away from landfill and incineration and toward AD.

And, most interestingly, this shift is expected to require an additional 150 to 200 new AD plants across the UK to handle the significantly increased volume of clean, segregated feedstock.

However, the Green Gas Support Scheme (GGSS), an initiative created by the Green Gas Levy (GGL) and existing to provide 15 years of tariff support to new AD biomethane plants is closing its books to new applications in 2028 and will officially end in 2030, causing uncertainty in the market as, currently, there have been no new initiatives announced or even hinted at to take its place.

With only 2 years left of the current scheme, developers, investors, and contractors are increasingly conscious that the next phase of UK renewable gas policy will shape project pipelines, financing structures, and construction timelines for years to come; breeding caution and hesitancy across the board – they’re understandably cautious to move forward with builds if they don’t know what support, if any, they’ll get! .

This “spanner in the works” makes the 2026 Simpler Recycling mandate feels like a paradox:

On one hand, the government is forcing 10 million tonnes of feedstock into the market; on the other, the primary subsidy mechanism for injecting that gas into the grid is sunsetting.

Without a “GGSS 2.0” or a similar revenue support model, the practicalities of delivering 150–200 new plants becomes a massive commercial challenge.

RTFO as a Strategic Alternative to GGSS

That being said, there is a ‘strategic alternative’ to GGSS available, RTFO A.K.A the Renewable Transport Fuel Obligation, which allows biomethane producers to step away from gas injection and towards transport.

Where we can think of GGSS more like a salary, RTFO acts like a market-driven commission that rises and falls based on market value, a bit like the stock market, allowing biomethane producers to access an alternative market and sell into the transport sector where the financial rewards can be significantly higher.

The initiative works on a system of certificates (RTFC) sold on from biomethane producers, i.e. AD plants, to fossil fuel suppliers in order that those suppliers meet their legal obligations regarding the percentage of renewables sold; that is, under UK law, companies that sell fossil fuels, like petrol or diesel, must ensure that a certain percentage of their sales come from renewables, and they do this by purchasing RTFCs from biomethane producers.

This pathway to market can be particularly attractive as RTFC prices have shown a general upward trend over the past two years, rising from approximately 15 p/RTFC in early 2024 to the current 25.60 p, and the scheme is running until 2032, 4 years beyond the 2028 GGSS cut off.

This, however, does come with some complications as biomethane producers generally can’t choose both pathways and must only choose one: GGSS or RTFO – grid or transport, where there are pros and cons for either.

The Novel Third Pathway To Market

And, of course, this wouldn’t be a waste to energy, PWCL article without touching on the opportunities afforded biomethane producers via Carbon Capture, Usage and Storage (CCUS) which enables carbon emitting plants to capture the CO2 emitted during the process of converting waste to energy, and store it and/or sell it on to other industries for use in their manufacturing processes, such as the food & beverage industry.

The Multi-Stream Revenue Model

What these pathways demonstrate is that modern Anaerobic Digestion has evolved far beyond a simple “waste disposal” process; it is now a sophisticated, multi-commodity energy refinery.

By navigating the choice between the GGSS (stable heat revenue) and the RTFO (high-value transport credits), and augmenting either with biogenic CO2 sales through CCUS, operators can build a “stacked” revenue model that is resilient to market volatility.

This commercial diversity is the sector’s greatest strength; it allows a single facility to pivot its output to wherever the UK’s energy need is greatest, whether that is heating homes, decarbonizing heavy haulage, or supplying the food and beverage industry.

In a post-subsidy world, this flexibility turns any small AD plant from a risky infrastructure build into a high-utility asset that can weather the “Spanner in the Works” and provide a bankable alternative to the declining North Sea.

Resource Efficiency and The Real Energy Trade

The tension between Conway’s Sky News analysis and the UK’s Net Zero ambitions is palpable and certainly spotlights a startling reality: we are currently choosing to trade domestic energy security for carbon-intensive imports to diversify energy sources, meet demand not covered by domestic North Sea production and Norwegian pipelines, and ensure our energy security.

However, the solution isn’t necessarily a binary choice between “drill more” or “freeze.” The real insight lies in resource efficiency and utilising the tools we have in our own, domestic “toolbox” to maximise our energy output.

If the industry scales to the projected 120 TWh, we are essentially discovering a new, renewable gas field every year and, unlike the 20% of “hard to reach” North Sea gas, food waste is a “ready-to-reach” feedstock already sitting in our bins; AD and EfW are “Right Now” technologies, and biomethane is a “drop-in” fuel that solves the carbon footprint of heating today and in the future without requiring every UK household to spend £10,000 on a heat pump or millions on additional infrastructure upgrades.

We just need the government to show confidence in the AD sector and, indeed, EfW and give us another GGSS-like initiative that extends beyond 2035; giving the sector something tangible and long term that acknowledges Energy from Waste’s crucial place in the UK’s long term energy security strategy.

From Disposal to Dispatchable Power

Ed Conway’s analysis for Sky News serves as a sobering reminder: the UK’s transition is currently leaving a hole that expensive, high-carbon LNG is all too happy to fill.

While the debate over North Sea licenses continues to dominate headlines, the “Gas Gap” doesn’t have to be a permanent scar on our energy security.

By April 2026, the UK will stand at a crossroads: we can continue to view our 10 million tonnes of food waste as a disposal problem – a “wet” burden that hampers our Energy from Waste plants – or we can view it as a strategic energy reserve.

If we can solve the “GGSS Paradox” and provide the investment certainty the AD sector craves, we won’t just be “sitting on more gas” in the North Sea; we’ll be generating it in our own backyards.

The transition to a clean energy future doesn’t require us to choose between the environment and the economy, it simply requires us to stop wasting the energy we already have.